Income Fund Update - Q4 2021

Hello Partners,

We’re off to a great start. We achieved our primary goal in 2021: high monthly income.

The annualized distribution yield for December was 12.1%.

The average distribution yield for 2021 was 9.4%.

Below are the full Q4 returns for the Income Fund.

Our overweight positioning on industrial, storage, and single family rentals paid off last year.

Our biggest sector miss was retail, which surprisingly outperformed on the back of strong consumer balance sheets thanks to unprecedented government stimulus.

Whiffing on a couple sectors per year will be a common theme. Our long-term strategy and focus on “sticky” tenants + cash flow growth means we’ll occasionally miss out on shorter term value trades.

Case in point - In 2022 I suspect our biggest sector miss will be office, which screens cheap today (for obvious reasons) and should benefit from COVID reopening. However, we’ll likely always be underweight office relative to the market. Office is a bad business with sky high capital costs and fair-weather tenants. We want to be consistently overweight great real estate business models.

2022 - Real Estate Market Color

The reversal of the COVID re-opening trade and the sell-off underway in the Treasury market has not been good for the lowest yielding REITs (highest quality real estate) in early 2022.

REITs trading at lower implied cap rates have underperformed REITs trading at higher implied cap rates1. Typically the opposite is true.

(we own VICI of these labeled REITs)

REITs will always have a knee jerk negative reaction to interest rate hikes. However, more often than not, REITs actually outperform during rising interest rate environments.

Between 2004 and mid-2006, the Fed hiked interest rates 17 times (from 1.0% to 5.25%) amid an improving economy. The month of that first rate hike announcement, REITs took a quick 15% loss (ouch), which was a top ten worst monthly return for REITs.

However, the following month REITs quickly rebounded, climbing ~80% in two years as the economy grew. History suggests that the health of the economy and the ability of REITs to raise rents typically outweighs rising interest rates.

In other words, it matters why rates are rising (growing economy vs. stagflation).

Of course, I can’t predict how REITs will perform this Fed tightening cycle. Therefore, we’ll continue to focus on income growth and individual REIT valuations.

If 2022 goes the wrong way, that’s fine too. We know the values (multiple on cash flow) will eventually follow income growth over a long enough holding periods.

Thankfully, our monthly dividends are a great reminder to keep this real estate owner mentality, stay the course and let the cash flow compound.

Investment Themes for 2022

1. Back to normal; it’s time.

New variant or not, life goes on. People will largely revert back 2019 behavior, covid be damned.

2. Real Estate as a replacement for bonds.

Private equity firms are still raising record amounts of capital monthly. Endowments and pension funds are increasing their allocations to private real estate as a replacement for fixed income. We believe this wall of capital will help provide a ballast against rising rate pressures in the private market.

2. Historic Consumer Wealth2

This bodes well for above average rent growth in most real estate sectors including some of our favorites: Industrial, manufactured housing, single family rentals, medical office, life science.

3. Inflation Fight

We got the higher inflation call right back in early 2021.

The Fed has now backed itself into a corner. Their plan is to slowly pull away the punch bowl with both bond tapering and perhaps four rate rises in 2022. However, their balance sheet is now ~$9 trillion. Can they reduce treasury holdings and raise rates enough to dramatically curtail inflation while avoiding a recession?

Who knows, but I’d assume they’d prefer the lessor of two evils (a bit above average inflation) and will let the economy run a bit hot longer, which helps reduce the national debt in real terms (a pernicious form of taxation).

How do we continue to position ourselves for the possibility of higher inflation? Thankfully we don’t have to do much. Our base strategy - overweighting assets with sticky tenants - is well aligned for periods of sustained inflation. Landlords with pricing power can typically push through rent increases in excess of inflation.

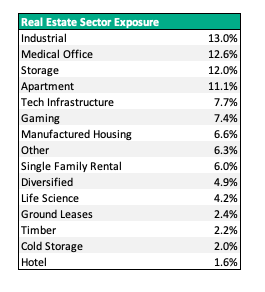

Fund Sector Weights

Over time, large differences typically exist in the total returns generated across REIT property sectors. We start with sector selection then try to pick the best and highest returning real estate given current prices.

Our largest sector weighting is a close tie between medical office and industrial. We sold most of the largest industrial REIT (Prologis) in December as its multiple shot up to a nosebleed 40x in December.

Therefore we favor the smaller / mid cap industrial firms (with strong development pipelines). Given the fundamentals, we expect one of our industrial holdings will get acquired in the next couple of years. There is still a lot to love about industrial given everything I noted in the Q3 letter.

Industrial rents are projected to grow double digits again in 2022. Industrial tenants are valuing the proximity to end customers far higher than the growing costs to operate their warehouses.

Portfolio sector weight as of 12/31/21:

We’ll share some updated market thoughts on our other overweight sectors in subsequent quarters.

Operational Notes:

All investors should have a portal account set up for them by now. If you did not receive log in info, please let us know and we’ll have the fund admin reach out to you.

Regardless of any rate-induced volatility we may or may not see in 2022, I remain confident in the long-term future of our portfolio, our ability to drive monthly income and our “sticky” tenants + cash flow growth strategy.

I encourage partners who are considering investing additional capital to reach out (as well as potential partners interested in joining our Evergreen Real Income Fund).

Best,

Brad Johnson

EVERGREEN

530 Technology Drive | Suite 100 | Irvine, California 92618 | www.evergreencap.com

Green Street Research

Blackstone - “Loans” represent home mortgages, commercial mortgages, consumer credit, depository institution loans, and other loans and advances held by households and nonprofit organizations.