Q4 2023 Update

Q4 2023 Update

Hello Partners,

I hope this update finds you well.

The average distribution yield for 2023 was 8.1%.

Below are the YTD & historical returns for the Income Fund though year-end.

We finished Q4 strong with a 13% increase that put us in the black (positive returns) for 2023. This boost was largely due to the continued decline in inflation along with the Fed’s admission that interest rate cuts are likely on the horizon.

From our 2022 Year End Letter:

We previously noted that in the early stages of a REIT recover we might leave some money on the table by not owning the most highly leveraged REITs in the most decimated sectors.

That’s exactly what happened late last year. Our higher quality holdings did not appreciate as much as the highly leveraged, lower quality, or left for dead (office) REITs when the market started to anticipate future rate cuts.

This is a temporary negative of our strategy. In other words, we’re not going to “chase” the market by changing strategies and buying lower quality.

Our Income Fund’s goal is to earn higher monthly income than our index or bonds.

That focus on income means we’ll occasionally underperform when markets are booming. However, we should make up for it by outperforming in most flat or down markets.

Market Outlook for REITS

It might be bumpy along the way, but REITs are positioned for further recover in 2024:

For obvious reasons, real estate has historically benefited from a monetary policy shift from tightening to loosening.

We suspect large REIT M&A transactions to resume in 2024. There was already a REIT take private purchase in January that we benefited from - We owned Tricon Residential, a single family home rental portfolio that Blackstone is attempting to take private at ~30% premium. We sold immediately on the news earning a 28% increase that day (I don’t like to wait around to see if the merger actually goes through just to earn a few more pennies per share).

The demand and supply equation looks promising in all sectors but office and southeastern apartments (further discussion in the next section).

Many REIT sectors still trade at a discount to private market net asset values (NAV), when historically the best sectors trade at a premium to NAV (to account for lower leverage, liquidity and overall platform value of the team). See below for recent NAV discounts.

Supply Picture

I spend a disproportionate amount of time thinking about supply constraints and maintenance capital.

Because - over the long-term - it’s new competition and large capital expenses that kill cash flow, not fluctuations in interest rates.

REITs that fail on both fronts tread water because they have to consistently issue new shares (which dilutes existing shareholders) to fund new acquisitions.

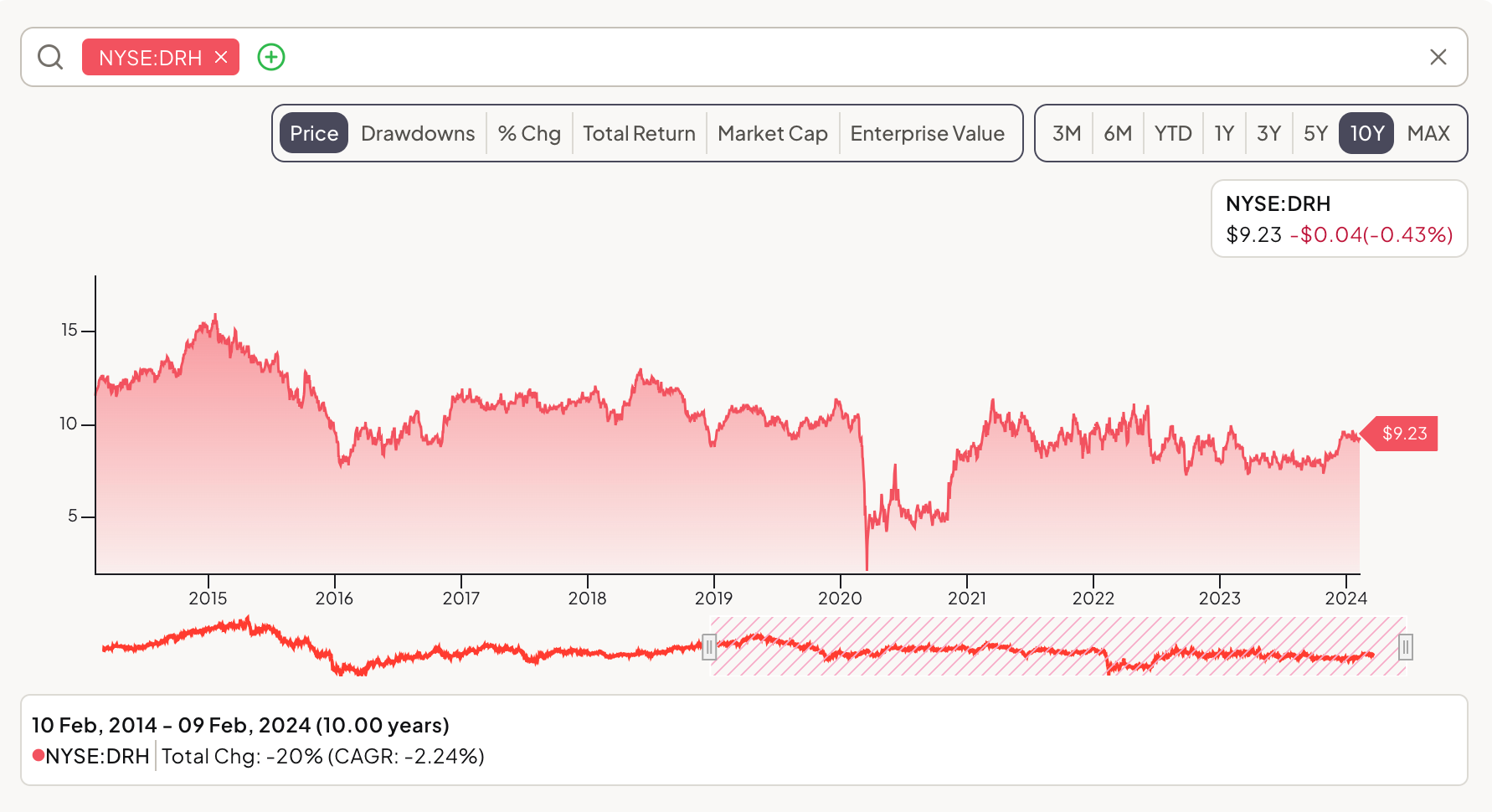

Case in point - here is DiamondRock Hospitality, a poorly run hotel REIT that hasn’t made shareholders money in a decade.

Why? Comments about the management team aside, their properties face a steady stream of new competitors (including Airbnb inventory) and must consistently renovate their buildings to keep up with changing customer tastes. It’s a brutal business.

We want the opposite of that.

Thankfully, due to the increase in interest rates and the dramatic spike in construction costs, there should be minimal new construction completions across most REIT sectors in late 2024 through 2026. Regional banks are in crisis mode and are not funding new construction loans.

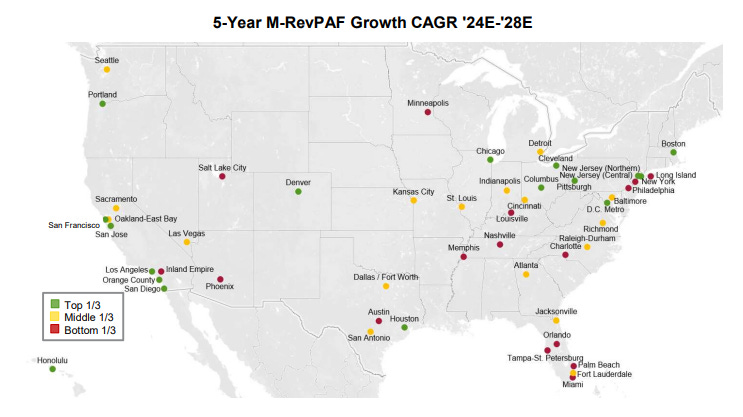

Other than office, apartments are the only sector with a near-term supply problem. There were record new deliveries in the SouthEast this year, but new apartment deliveries should drop off a cliff in 2025, which will enable apartment owners to start pushing rent increases again.

Here is a map that shows markets that are facing the most new apartment supply headwinds. “M-RevPAF Growth” combines occupancy growth and rent growth. New York is typically a supply-constrained costal market that mirrors west coast apartment performance, but the wild card there is the amount of class b / c office properties that will be converted to apartments.

However, excluding office and apartments, the supply picture looks solid across other real estate sectors.

Therefore, I believe most real estate is in an enviable position over the next two years given the two likely outcomes with the economy:

If the economy softens, the Fed will reduce rates deeper than anticipated, boosting REIT and real estate values.

If the economy continues to hum along, tenant demand growth (without the associated spike in supply) should lead to above average rent growth over the next few years.

REIT Sector Outlooks

We continue to favor REIT sectors with sustained growth drivers, low ongoing capital expenses and some degree of pricing power due to supply / demand imbalances.

REIT Sectors by Cap Ex and Growth:

As you can see from this list, there are some clear losers we’ll be avoiding (or at least heavily underweight in 2024).

Underweight:

Hotel REITs - we’d rather own a highly profitable hotel asset management business like Hilton (a high-quality, great business with high returns on capital) vs. the actual hotel properties, that require tons of labor and capital to maintain.

Office - for obvious reasons. Office sector delinquencies remain well below historical highs of 2012 and 2013. Most would assume GFC defaults would have peaked in 2010, but distress takes a long time to filter through real estate with long-term leases. Office delinquencies will get worse before getting better.

Net Lease - net lease deals (where you pass through all expenses to the tenants) require almost no ongoing capital, which is great. However, while there are a couple exceptions, most net lease REITs (that own small fast food pads, gas stations or convenience stores) won’t be attractive until they can issue equity cheaper than it costs to buy real estate. That’s how they drive growth. They are acquisition machines.

Overweight

Industrial REITs - Despite short-term caution due to normalizing demand and an anticipated surge in supply in early 2024, their long-term outlook remains positive. Factors such as e-commerce expansion, last-mile distribution and re-shoring support this optimism.

Wireless Tower - Cell Towers show promise thanks largely to the relentless growth in mobile data and the deployment of next-gen technologies like 5G, which requires additional wireless communications infrastructure. Our favorite holding here is American Tower, which is a world-class company operating one of the best business models ever created, trading below its 10 year average multiple. This is attractive considering the world’s obsession with cell phones and increased data usage. Hard to imagine the world using less data anytime soon.

Self-Storage - Self-storage is another unreal business model, with the largest self storage REITs operating at 70%+ gross margins. This sector underperformed in 2023 due to dramatic decline in home sales. Our largest holding in this sector is Public Storage. We anticipate improved valuations and fundamentals in the coming years.

I’ve owned a few self storage assets and they are an dream to operate vs. apartments.

Tenants stay far longer than you’d expect

Tenants don’t wear down the units or common areas

They offer inflation protection - ability to change rent monthly

They have low ongoing capital needs - the steel frames and roll-up doors cost next to nothing to maintain.

This enables storage REITs to gush cash flow. They can keep growing their dividend and still deploy excess cash flow into new acquisitions, which compounds capital.

Manufactured Housing - Our favorite investments in this sector include Sun Communities and Equity Lifestyle Properties. Both REITs are poised to capitalize on favorable demand-supply conditions and are projected to derive benefit from persistent demand coupled with a lack of new inventory from high development hurdles. These companies are well-positioned for long-term revenue growth.

Health Care - Our confidence in Ventas rests on the promising future of senior housing, propelled by demographic trends and an aging population. Senior housing properties are witnessing improved fundamentals with controlled supply and lessening labor cost pressures.

Data Centers - While pricing is not as attractive as last year, the sector's prospects are bolstered by the near insatiable tenant demand fueled by cloud computing and AI. Our largest holding here is Equinix, which owns most of the most valuable datacenters in the world (interconnection dense locations that serve as mission-critical facilities for the mega tech companies). They facilitate 462,000 separate interconnections between network companies that help the internet function. This real estate has a massive, irreplaceable moat as these businesses can’t operate without these connections.

Economic Backdrop:

At the start of the 2023, the overwhelming consensus among economists anticipated a recession. In our 2022 year-end letter we cast doubts on that certainty given the strength of the job market and excess consumer savings, which is dwindling but still supports consumer spending.

So while we dodged a widespread recession in 2023, the real estate sector experienced a severe contraction, with private property values plunging by 20-40%—amounts comparable to, or in certain cases more severe than, the financial crisis in 2008.

REIT declines in 2022 were the canary in the coal mine for the private market pain felt by real estate owners last year.

As we look ahead to 2024, optimism continues to guide our outlook. There are obviously potential risks from geopolitical tensions, temporary hiccups the inflation figures and the delayed economic impact of past interest rate hikes.

However, there are several compelling reasons why we maintain a positive stance:

A stubbornly low unemployment rate of 3.7% - with 1.4 jobs available for every unemployed person.

Continued disinflation and increasing consumer purchasing power, with wage growth at 4% surpassing inflation rates for the first time since early 2021.

Monetary Policy Shift: While we hate making interest rate predictions, given the glut of global debt, we do expect global central banks to cut interest rates, providing relief for consumers, businesses and government interest payments. We suspect there will be fewer US rate cuts than the market thinks, but we certainly won’t be investing on the basis of such guesswork.

So What?

We continue to believe the long-term case for REITs remains compelling as publicly traded real estate offers:

Above average income

Little risk of distress vs. one off private real estate deals, many of which purchased with floating rate loans in 2021-2022 are facing severe challenges today

Diversification and historically lower correlation to equities

Strong long-term returns relative to most investment alternatives

Therefore, we’ll continue to stick to the plan and hold high caliber, income producing assets.