Income Fund Update - Q4 2022

Income Fund Update - Q4 2022

Hello Partners,

Hope this update finds you well.

The average distribution yield for 2022 was 8.8%.

Below are the 2022 returns for the Income Fund.

Real estate fundamentals were stellar in 2022 yet REITs suffered their 2nd worst yearly performance ever.

Not to be outdone, bonds put up their worst performance in 250 years.

Why?

Inflation climbed to a 40-year high and the Fed funds rate went vertical. The unprecedented speed of the Fed's rate increases created pain for all assets; but especially income investments.

The fund was down 19.6% vs. a negative 25.1% for the index in 2022. It’s good to outperform our peers, but I hate negative years. Downside volatility is never fun, but it’s part of the process and helps us buy real estate on sale.

We’ll see what 2023/2024 brings, but history suggests that REITs are well positioned.

Recession Rebound?

Is a recession inevitable or did the Fed thread the needle with a soft landing? Your guess is as good as mine.

But if we’re destined for a recession, REITs still look compelling vs. private real estate over the next two years.

Below are the average total returns for pubic and private real estate before, during and after the last six recessions.

Source: Bloomberg, NAREIT, NCREIF, as of Jan 19th 2023.

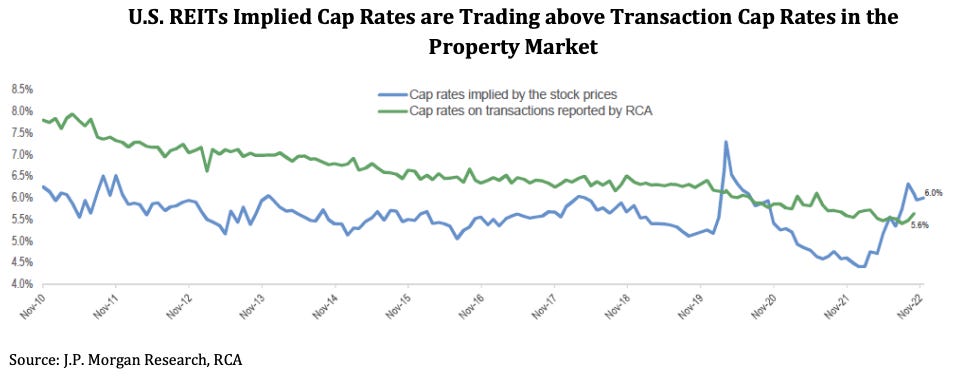

Why Should REITs Outperform?

REITs took their medicine in 2022, while private appraisals lag and some property owners are still in denial.

Most REITs have superior balance sheets, multiple funding options and can go on offensive while many private owners deal with loan refinance issues.

Sector Selection

The goal is to get our capital in the right real estate - at a reasonable price - and let the cash flow do the heavy lifting (price will catch up).

A large part of our above process is sector selection.

As you can see below, there is a substantial performance gap between sectors each year.

The average yearly gap (between the best and worst performing sectors) is ~40%.

Most years we expect to have a high batting average on sector selection. Last year we did ok, but not great.

Reason being, everything sold off last year - regardless of quality. In bear markets correlations converge to one (aka everything tanks). 2022 was the only year that happened on the above chart.

Fund Positioning

As we mentioned in a prior update, if 2022 was about inflation & interest rates, 2023 should be about earnings. I think that still holds true.

Therefore, our portfolio is geared a bit defensively towards high quality real estate with predictable earnings growth.

Those sectors include:

Industrial - huge embedded rent growth, on-shoring tailwinds

Medical Office - recession resistant, stable demand

Manufactured Housing - recession resistant

Grocery Anchored Retail - recession resistant, stable demand

Infrastructure - recession resistant, strong demand tailwinds

Life Science - sticky tenant base, strong demand tailwinds

Self storage (normally recession resistant) and multifamily are trading at discounts to private assets but they are both coming off unreal rent increase runs the last two years.

We remain bullish on both sectors long-term, but these are tougher to handicap vs. market expectations if we have a harder landing / recession. We will likely be underweight or neutral on these sectors until we have more clarity on demand.

Excluding periods of extreme valuations, we typically have zero exposure to bad business models (ex: office, hotels, malls, which all require HUGE never-ending capital improvements just to maintain rents).

Vacation Yes….Subway No

Office is still in trouble. Well, at least large costal office portfolios (ex: NYC, SF, LA).

Three office REITs recently announced pending dividend cuts. SL Green (SLG) announced a 13% decrease for its January 2023 distribution. Vornado (VNO) stated it would likely cut its dividend in 2023. Los Angeles focused Douglas Emmett (DEI), just reduced its dividend by 32%.

While their newer trophy assets are fine, their older / commodity offices are in a slow burn. They have to cut rents to keep existing tenants and they have to offer huge tenant improvement + free rent packages to attract new tenants. If you account for these big capital expenses (which most don’t) office REITs are highly levered and still not cheap.

Declining operating fundamentals + high leverage + maturing debt is not a great combo.

Now throw in a possible recession with further job losses, a mountain of sublease space and the completion of some large new office towers to increase supply.

Rough setup. We believe the best office portfolios will recover, but it’s likely to take longer than most people think. Most office REITs are expensive relative to the huge headwinds they are facing. The portfolio still has a small net short office position.

Kastle Office Occupancy Report

Conclusion

REIT valuations are attractive and balance sheets are stronger than ever.

I believe the portfolio owns world-class real estate companies with a lot of embedded earnings growth and is well positioned to capitalize on a rebound over the next 1-2 years.

Thank you,

Brad