Income Fund Update - Q2 2023

Income Fund Update - Q2 2023

Hello Partners,

Hope this update finds you well.

The average distribution yield for 2023 YTD is 7.9%.

Below are the YTD & historical returns for the Income Fund along with a summary of one of our core holdings, Rexford Industrial.

2023 has been a choppy year for real estate yet nothing has changed on our positive long-term outlook for public REITs and real estate-related securities. Our confidence is rooted in several factors:

We expect low levels of new construction activity to continue, which is a favorable comparison to past real estate cycles marked by overbuilding and subsequent declines.

Balance sheets across the sector are still extremely strong, with record low leverage levels, staggered debt maturities and little to no floating rate debt.

Our favorite holdings are undervalued vs. their long-term multiples and (more importantly) vs. private market values.

All and all, the current real estate environment is far superior than in previous cycles, which were defined by overbuilding and sky high-leverage. Therefore, we believe our Income Fund boasts a promising return prospect over the coming years, with a favorable risk-reward balance.

Industrial

Our largest sector exposure remains industrial (~15% of the fund).

We are still seeing unprecedented strength in industrial. The push by consumers for a “2-hour” vs “2-day” delivery is accelerating demand for well-located warehouses. I don’t think this trend is going to reverse. Americans want their stuff and they want it now.

The secular shift to last-mile logistics coupled with the on-shoring of manufacturing has resulted in record low vacancy of 3% and new leases signed at 40%+ higher rents than expiring leases across the best industrial portfolios.

Core Holding - Rexford Industrial

Rexford Industrial is one of our favorite REITs and is our largest industrial position. The company is focused exclusively on driving shareholder value by investing in industrial properties within infill Southern California locations.

Rexford carries a fortress balance sheet and owns an irreplaceable portfolio in the nation’s largest, most sought after industrial property market.

Plenty of private equity groups would give their right arm for this portfolio. Despite this, Rexford currently trading at a ~18% discount to it’s private market value.

This is both the great and occasionally frustrating part about public investing (depending if we want to keep buying, or if we’re already fully invested in a position).

But since we can’t control when Mr. Market will get around to fixing price discrepancies, we focus on the real estate fundamentals. Which in the case of Rexford, are unreal.

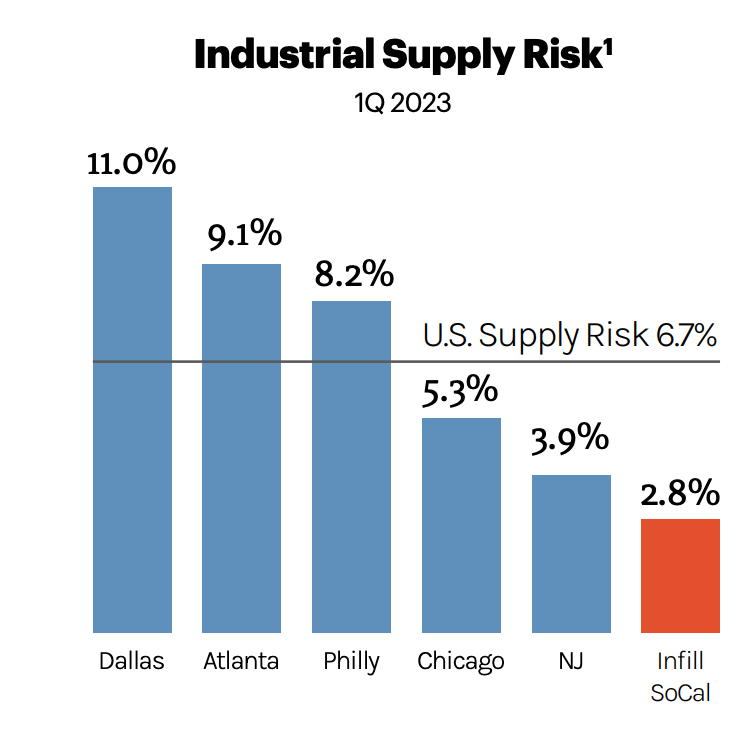

Highest Barrier Market

Southern California represents the largest logistics market in the US and is one of the top 5 markets globally. The region boasts a vast and diverse economy, supported by a population of approximately 21 million residents and over 600,000 businesses.

Needless to say, it’s crowded here.

I live in Orange County and have spent most of my life in Southern CA.

While there is more space inland, there is almost nowhere left to build warehouses in LA or OC (Rexford’s primary submarkets). Consequently, Southern California stands out with consistently lower vacancy rates across all economic cycles largely because it has the lowest new supply risk in the country.

The inability to materially increase net supply insulates Rexford's portfolio more than other less restrictive U.S. markets.

Barriers to new development in Southern California:

Sky high cost of land per acre

Restrictive zoning (only affordable housing getting approved)

Permanent natural barriers (oceans, mountains, protected land)

Adding to the supply-demand imbalance, Southern California experiences diminishing supply as industrial properties are occasionally converted to other (higher and better) uses. This trend further exacerbates the scarcity of industrial real estate in the area.

As you know, we love real estate with high hurdles to new supply.

Because despite what the headlines may say, it’s oversupply that causes existential threats (permanent loss) for conservatively leveraged real estate. While value fluctuations caused by recessions or interest rate volatility tend to be temporary.

Rexford Has Already Won

Real estate is not complicated.

If you have high demand and new competitors can’t enter your market, good things are going to happen.

Rexford is already the dominate industrial owner in this infill market. They have the deepest acquisition team in the region and the most established broker relationships. They also have permanent capital with no need to sell. These assets are going to deliver high cash flow for a long time.

Unlike many other of our holdings, Rexford doesn’t look cheap at first glance (despite being down ~35% since its all time high in 2022, when it was NOT a core holding for the fund).

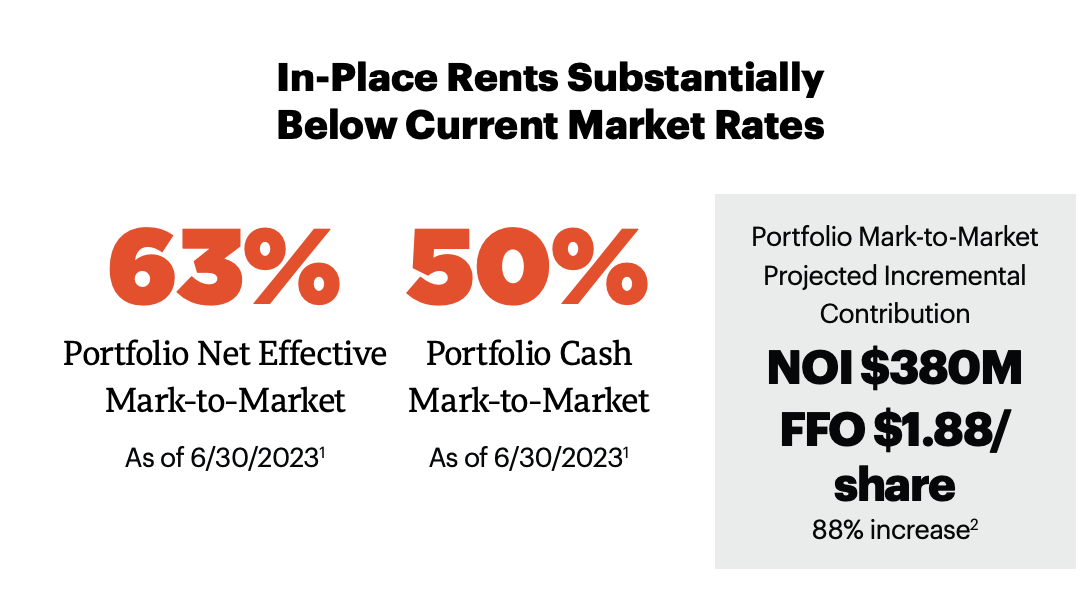

However, they are sitting on a large asset: a ton of embedded rent growth which should be unlocked as current leases roll to market.

Rexford's current lease rents are considerably lower than market rates, presenting an opportunity for sustained cash flow growth. As of Q2 2023, new leases are still being signed at staggering 75% higher rates than in-place rents.

By adjusting rents to market levels over the next few years, the company anticipates achieving 60%+ cash flow growth. That is a healthy margin of error to offset even the most draconian recessionary projections.

Overall, Rexford stands out as having one of the highest growth potentials among all publicly traded REITs. Alongside Rexford, other industrial REIT holdings in the fund, such First Industrial Realty Trust, Inc., should also benefit from the positive market conditions and the potential for high demand and long-term rent growth in the industrial sector.

The quoted price for this irreplaceable portfolio is going to move around. Inflation or recession fears could certainly discount it a bit further.

Regardless, if I could own one regionally focused portfolio in America this would be it. Consequently, Rexford is one of our core holdings.

Thank you,

Brad Johnson

Evergreen Capital