Income Fund Update - Q1 2022

Income Fund Update - Q1 2022

Hello Partners,

Hope this update finds you well.

The average distribution yield for Q1 2022 was 9.7%.

Below are the full Q1 returns for the Income Fund.

2022 has not been kind to the market thus far. Recession concerns, Ukraine, inflation, rising rates, tech meltdown, etc.

Consumer sentiment is low and volatility is high. The Nasdaq just had its worst month since 2008.

REITs are also down, yet Q1 earnings were better than expected. Among the 33 REITs that provided full-year guidance, 27 REITs (82%) raised their growth outlook for the year. Stellar fundamentals are not enough to offset interest rate concerns early in a Fed rate-rising cycle.

Growth-oriented REITs - our favorite core holdings - suffered the worst on interest rate worries. Tech friendly sectors, including industrial (–6.1%) and digital infrastructure (–12.4%) were down as investors rotated out of growth. Single-family rentals (–9.9%) and manufactured housing (–14.5%) also underperformed. Long-term we’re bullish on all of these sectors.

Real Estate Market Color

In the private markets, property prices have plateaued.

Bidding wars are still happening, but there are rumblings of price adjustments and deals falling out of contract due to rate increases. Buyer demand for assets isn’t going anywhere, but some of the froth is gone.

As of today, REITs have priced in a modest discount to the private market, we’ll see which market is right over the next 6-12 months.

Inflation

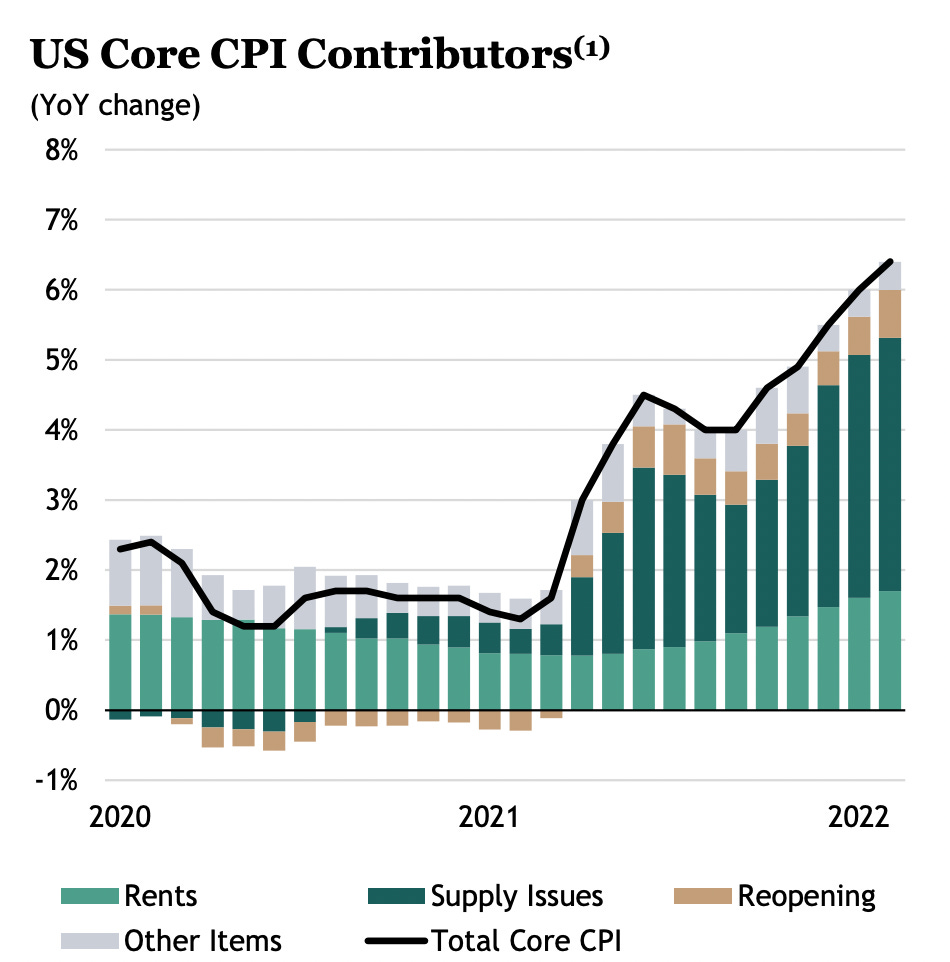

Headline inflation numbers seem likely to peak in next few months. This is largely due to base effects. Inflation will still be high short-term, but new numbers are being compared to already high numbers from 1 year ago (see chart below) therefore the rate of change comparison should soon start slow / decrease soon.

As previously written, I’ve long assumed inflation will run above average over at least the near term. However - China’s lockdown notwithstanding - the supply problems (bulk of inflation today1) should eventually soften and we all know the cure for high prices is…high prices. The recent rent increases though - which are a large component of core CPI - are not fully baked in, which should keep inflation above average for longer.

If history rhymes, persistent inflation should benefit our core REIT holdings over the medium term 2-3 years as they:

can typically raise rents faster than their expenses grow

are insulated from oversupply due to soaring development costs

have incredibly cheap, long-term, fixed rate debt (an amazing asset during high inflation as the fixed rate debt melts away)

Cost of Capital + Pricing Power = Superpower

One of the major benefits of investing in world class REITs relative to private real estate is cheap money.

One of our holdings, Equinix (the largest datacenter REIT + tollbooth for global internet traffic), just announced its 77th consecutive quarter of revenue growth with record net bookings. It’s a cash printing machine.

The company’s scale and consistency enables them to tap the debt markets at terms mere mortal real estate investors would kill for.

Equinix has an effective interest rate of 1.7% on $11 billion dollars of fixed rate debt with ~9 years of term remaining.

Their debt is sub 2%, yet they growing total cash flows like clockwork at 8-9%. Not a bad game to play.

Having access to this type of debt in a rising interest rate / inflationary environment is both an offensive weapons (acquisitions) and a defensive moat.

Similar to Equinix, most of our REIT management teams have done an excellent job shoring up their balance sheets in preparation of a possible slowdown / rate rising world. Almost all have locked in extremely attractive, fixed rate date for the long-term. Most have sub 30% loan to value debt. Frankly, I wish they would have pushed leverage a little bit higher. At least we can take comfort knowing our REITs balance sheets have never been stronger.

Positioning

Who knows, but it seems like markets are in for more choppy waters 2022. The Nasdaq and most tech firms are in price discovery, which is a nice way of saying they’re tanking. Impossible to know what temporary second order effects that may or may not have on the broader market and our holdings.

As usual, we’ll focus on REITs that can grow our income and will flex position sizing up and down based on valuation multiples.

Fund’s Audit

The Audit report from Spicer Jefferies was just finalized. I included a temporary link in the email we just sent to you and we’ll see if the the fund administrator can upload it to the Portal (if you’d like to review).

TL;DR: The Auditor blessed the year end numbers prepared by our Fund Administrator.

Best,

Brad Johnson

EVERGREEN

530 Technology Drive | Suite 100 | Irvine, California 92618 | www.evergreencap.com

Blackstone, Bureau of Labor Statistics, and Haver Analytics, as of February 28, 2022